Productivity is variable in the short term and it is everything in the long run

In the Notes for Discussion 1-3, we discussed the demographic projections by the Hellenic Statistical Authority (ELSTAT) for the future population of Greece, the working-age population (15-64), and employment and unemployment. The argument was that the macroeconomy is anchored in the size of the population, and that if the population starts declining, then the size of the economy will be restricted. Since Greece is struggling with a legacy debt problem, a potentially smaller economy in the future is an important factor when thinking how best to manage the economy going forward and in particular the resolution of this debt problem. The first three notes focused on volume input of labor – by how many the number of employed persons may rise or fall in the future. A second variable that determines the potential size of the economy, or potential output, is how productive these future workers will be. The latter is the question of this Note as we delve into an analysis of labor productivity.

Economists say that “productivity is variable in the short run and it is everything in the long run.” What they mean is that the standard of living per person in the economy can only be lifted by productivity gains – how efficient the economy is in producing output per worker employed. Having visited many countries over the years and studied their economies, I have developed a rule of thumb, or a type of hypothesis, to start the analysis of productivity: The growth in labor productivity as a long-run average tends to be around 1.5 percent a year, and the growth in the related concept called “total factor productivity” or TFP in its long-run average is often around 1 percent a year.

Productivity numbers vary by country. And they are not constant year-by-year, either. However, countries that make these numbers as longer-run averages have done well over time, each within their normal cycles of ups and downs. In previous notes we “assumed” that Greece can also achieve a labor productivity growth of 1.5 percent a year as a long-run average. We can now use data from ELSTAT to see if there is any evidence for this rule of thumb for Greece.

ELSTAT very helpfully publishes a time series of quarterly data on real GDP and employment (number of persons). By dividing the level of output by the number of persons that worked to produce this output, we can derive an indicator of output per person employed – we will call this labor productivity. The growth rate over time in this variable is the number we are interested in – growth in labor productivity.

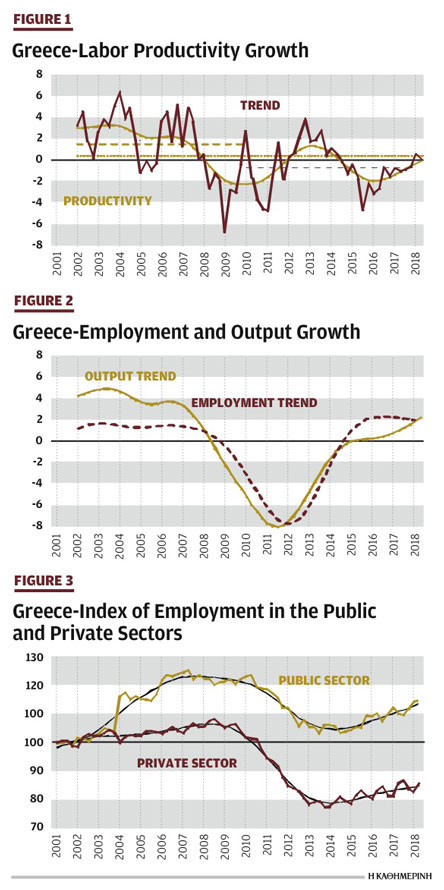

Figure 1 shows the results of this calculation. Allow me touch upon some observations that come to mind:

– The spiky solid red line shows quarterly productivity growth (over the same quarter of last year). Since the rate of variation is high (there is lots of noise in the signal), I have applied a statistical technique to derive an underlying trend line that separates the noise from the underlying signal – this is the solid, and more gradual yellow line in the picture. By none of these two measures is labor productivity a constant; we are mainly interested in longer-time averages.

– The horizontal upper dashed yellow line shows average productivity growth at 1.5 percent a year over the period 2001-2009. The horizontal lower dashed black line shows average productivity growth of -0.6 percent a year over the period 2010-2018Q2. And the horizontal dotted straight yellow line, in-between, at 0.4 percent a year, shows the average over the whole period 2001-2018Q2.

– Thus, over a period of 18 years, labor productivity only averaged 0.4 percent a year, far less than the 1.5 percent we assumed in the first two notes. But it should be recognized that this straddles a tremendous recession, and some significant brain drain by highly productive persons, which is not a normal time for the economy. Indeed, and interestingly, in the good years of the early 2000s, through the downcycle that already started in 2009, productivity growth did average precisely 1.5 percent. So, for about a decade, Greece averaged just about what one would aim at in the longer run (when talking about “structural cycles” as opposed to the more familiar “business cycle” we need to talk about one, two, or even three decades, not five-year periods).

– The yellow trend line of productivity growth is also interesting: It has a double dip. Things first started to deteriorate after 2007. This coincides with the beginning of the global financial crisis in the US in July 2007. The deterioration bottomed out with the first economic program in 2010, with measures to start improving the performance of the economy (even though it felt terrible for Greek people who only then were becoming fully aware of the challenges for the country). Then, at around 2012-2014, the productivity developments started to improve as its growth became positive again. But this was aborted at around 2015 and into 2016. This coincided with a “new approach” to negotiating with the European partners, assertive changes in policies, and a new collapse in confidence with the need to stem capital outflow with capital controls in the economy – productivity growth entered into a double dip as a result of these policies. In more recent years, the economy seems to have found some new confidence and trend productivity growth is just about to turn positive. This is new and hopeful progress, but there is still a long way to go to feel safely back around 1.5 percent productivity growth a year as a longer-term trend and it will take time to achieve this better number.

Bottom line: There is helpful information in Figure 1. Unfortunately, based on the available data, Greece is rather far away from the 1.5 percent a year assumption of the previous notes, but the dynamics of the situation seem to be improving again, gradually. We will return to a third calculation of “potential growth” based on the findings above, later.

There is further interesting information embedded in the data from ELSTAT. We can look at the dynamics of real output growth and growth in employment side-by-side. Recall that productivity is the ratio of output over employment, so both the numerator and the denominator are of interest. Figure 2 is designed to have a closer look.

In this figure, I show only the underlying smoothed signal, not the quarterly ups and downs, which are less informative. We see that the high productivity growth in the 2000s came primarily from high output growth in the 4 percent range – these were the good years. Employment grew at between 1 and 2 percent a year over this period. Then output growth started falling before hiring in the labor markets reacted to the more difficult times.

Economists say that “labor is a lagged variable,” which means that it reacts to economic cycles with a delay – very evident in this picture from 2008-2014. The reason is that business managers need time to see where the cycle is going and since hiring and firing is costly, they react with a lag to more fundamental information. Only when the business community realizes that the cycle is a true downturn that will take some time to play out will they start adjusting their human resources stock of employees.

The same normally happens on the upswing – at first productivity grows faster-than-average because output is recovering but businesses want to wait and see before they expand employment. This produces higher productivity and higher profits for firms. If there is confidence and business firms invest these profits to meet higher future demand, labor demand will follow with a lag. Thus, the normal pattern is that labor responds with a delay to cyclical movements in the economy.

The reading above is what makes the episode since about 2015 so interesting in the case of Greece: The labor market seems to be (at least temporarily) leading, and not following, the output recovery. What can explain this and is it sustainable?

My best guess is that a contributing factor was that when the SYRIZA government came into power, they were keen to (re-)hire more people. While this may make for good electoral politics, the economic risks are high, because if output growth does not catch up and starts to exceed the pace of hiring, or hiring takes place mostly in lower productivity jobs, then profitability in the economy will fall, investment will not be forthcoming or even decline, and a triple dip may be in the offing. We can see toward the end of the 2017-2018 period that employment growth is leveling off and output growth is catching up. This is good news, and the very favorable external conditions together with continuous patience of creditors and gradually returning confidence to find solutions for Greece may have contributed to make this possible.

So is there any evidence of accelerated public sector hiring suggested above, in the data? Here too we can benefit from the helpful long time series on employment published by ELSTAT. Figure 3 shows the results of the analysis of these data.

In Figure 3 I have taken overall employment and broken it up between the public sector and the private sector. Then I have constructed an index based on 2001Q1 = 100, so that we can see from this index how employment volumes evolved during the crisis in the public and private sector, respectively. Some observations may again be made:

– The public sector had a huge increase in employment in 2004, which must have been related to the Olympic Games (top lines). This increase was not reversed after the Olympics, and, in fact, another big increase followed in 2006 (possibly related to local elections). Public sector employment stayed some 23 percent higher than in early 2001 through Q2 of 2010. This is when the first economic program commenced and the need for cost reductions was driven home. The decline in public sector employment ended in Q3 of 2013; in 2014 the variation was mooted; but in 2015 hiring took off again, and the underlying pace of hiring has picked up somewhat as evidenced by the curving up of the smoothed trend line through the raw index data. In early 2018, public sector employment again stands some 15 percent above its level of early 2001. This is remarkable, given that the real GDP is smaller than in 2001, after suffering the deep recession.

– The figure also shows that hiring in the private sector was much more gradual during the boom years of the 2000s, but that the decline in employment in the private sector was much bigger than in the government and continued through 2014 (bottom lines). The recovery in private hiring since 2014 is slower than the recovery of hiring in the public sector in recent years because the gap between the two lines is widening.

– Since the public sector is now bigger, in relative terms, than the private sector, coming out of the big recession, labor resources have evidently been shifted from the private sector to the public sector. This is very counterintuitive for an economy that needs reforms to get productivity and output up. The public sector is an administrative and regulatory body, and the private sector is the productive body of the economy, so shifting resources from the private to the public sector is a strange policy to get the economy going again. It seems that the government wanted to “push” the recovery with a hiring impulse, but this will only work if the private sector can catch up with new growth. It is a risky strategy that will depend in part whether the favorable external conditions will last and give Greece a push in the back. Otherwise, this strategy may run into trouble before too long. It may also explain why there is such pressure in Greece to increase taxes on the private sector – to pay for the new hires in the public sector, to boost the primary surplus, and sundry spending initiatives.

– Conventional economics would recommend continued wage moderation and hiring moderation, if not an attrition policy for hiring in the public sector, until the economy has clearly left the crisis behind. Future data on employment trends and productivity gains will tell.

Some closing thoughts

– Labor productivity growth has averaged only 0.4 percent a year during the last two decades. It is now gradually improving again. The economy needs more effective reforms to improve efficiency and boost productivity. Complementing this analysis with the concept of labor productivity per hour worked, compared to per employee, might provide further useful insights as to what the economy is doing.

– Potential growth will be further restrained if higher productivity growth cannot be restored.

– “Pushing the economy” by accelerating hiring in the public sector seems a high-risk strategy. A safer, but perhaps initially slower, path would be to foster a smaller public sector and shift productive resources to the private sector.

– The public sector is relatively bigger than in 2001; the private sector is relatively smaller than in 2001. Thus, private employment has paid a higher price in the recession than public employment.

– It would appear that wage moderation and a hiring slowdown as well as enhancing efficiency in public service remain necessary to control costs (moderating the need for taxes) and improve productivity and fundamental competitiveness in the Greek economy.

– In the next Note for Discussion, we will look at a third measure of potential output growth, based on the productivity findings above (rather than using an assumption of a constant 1.5 percent a year). We can then compare this indicator of potential output with actual output to get a measure of the “output gap” that indicates how far from potential the economy has been, and how this output gap may close in the future. In turn, this concept of the output gap is important to calibrate expectations of what is to come and how to frame fiscal policy for sound macroeconomic performance.

Bob Traa is an independent economist. This is the fourth in a series of articles by him for Kathimerini titled “Notes for Discussion – Essays on the Greek Macroeconomy.”